Clear, comprehensive and actionable transaction data at your fingertips

The Intix Transaction Data Platform keeps you in control of a changing financial landscape by integrating all transaction data into one place. Access what you need at any time and give your customers and your team the power to make the best data-driven decisions.

Unlocking value throughout the transaction life cycle.

Why Intix?

We serve customers in more than 20 countries.

4 of the Top-10 European banks are powered by Intix.

We partner with FIS who work with 95% of the world’s leading banks.

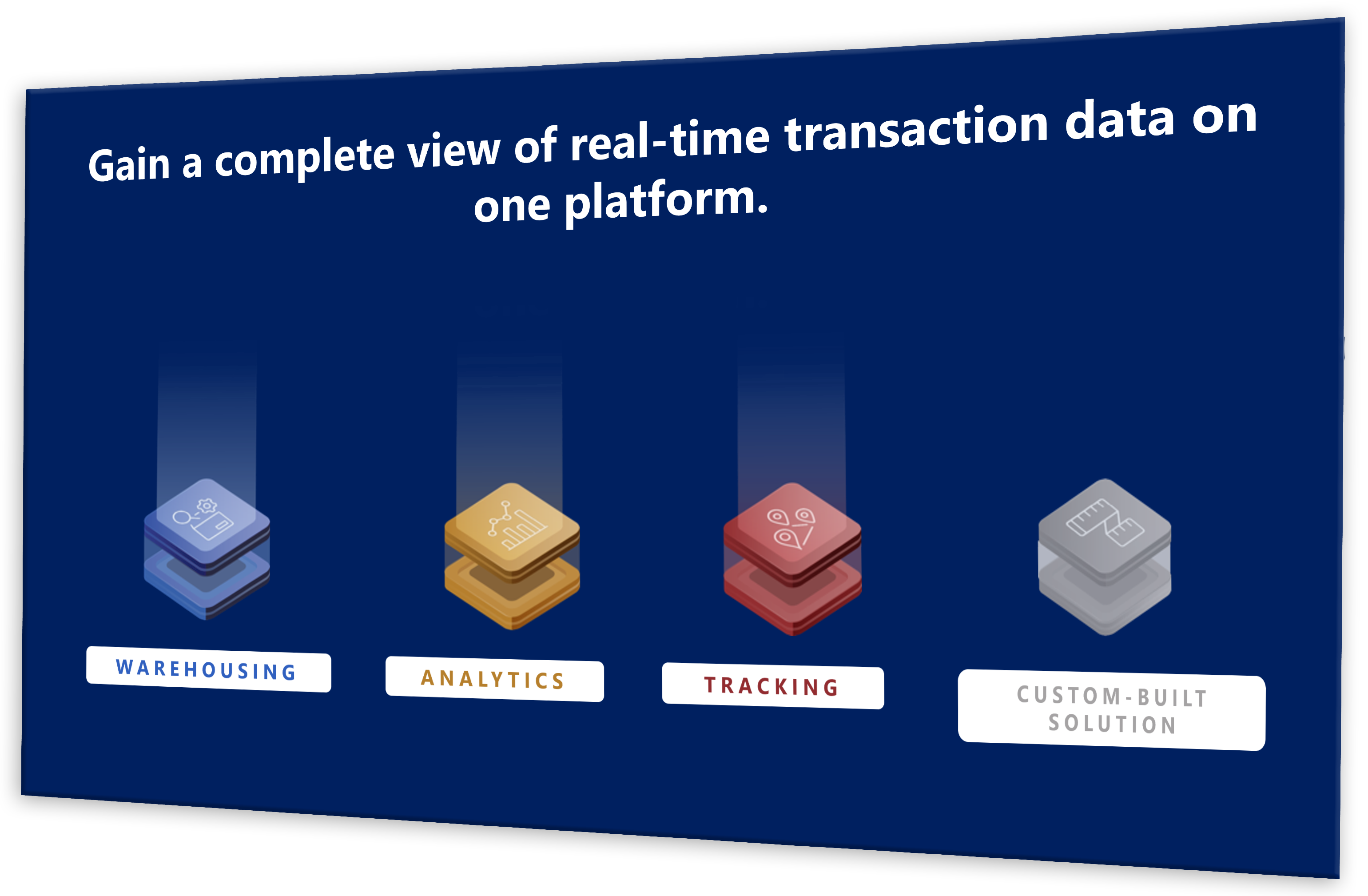

The Intix Transaction Data Platform enables our customers to

better manage, access, track, alert and analyse every transaction.

Discover our Case Studies

Clearstream selects Intix for Transaction Data Management

With the Intix solutions, we have all the relevant transaction data in one source, and we have gone from taking several hours to create different SQL statements to a near-time analysis.

Now everything is combined inside Intix, we have analytics running on top of it, and we are now in the position to give straight answers towards our customers, and by this have a much, much better time to market, and increase the satisfaction of our response.

Daniel Besse

CIO at Clearstream

Want to learn more through a Demo?

News & Resources

Financial data is a powerful tool for businesses. It offers insights that can help streamline op …

With the goal of advancing the financial crime prevention landscape, Intix and Ne …

In this episode of The Fintech Show, Fintech Finance News hosts FIS Head of International C …

We look forward to you joining our Webinar on Transforming Payment Services for the Digital Age: …

As part of its strategic growth and innovation-focused approach, Intix, a leader in transaction …

Summa Equity (“Summa”), a Stockholm-based private equity firm that invests in companies solving …

Learn more about our Transaction Data Platform

Explore the platform that unifies transaction data to empower your teams and delight your customers with new insights, streamlined compliance and efficient management.